The new Health and Social Care Levy – Increase in National Insurance and Dividend Tax from April 2022

The new Health and Social Care Levy – Increase in National Insurance and Dividend Tax from April 2022

Following the recent approval by the Government to the new Health and Social Care Levy : Increase in National Insurance and Dividend Tax, introduced to provide additional funding for social care costs following the COVID-19 pandemic, we have taken a closer look at the increases which will commence from 6 April 2022 and summarise the main points for you.

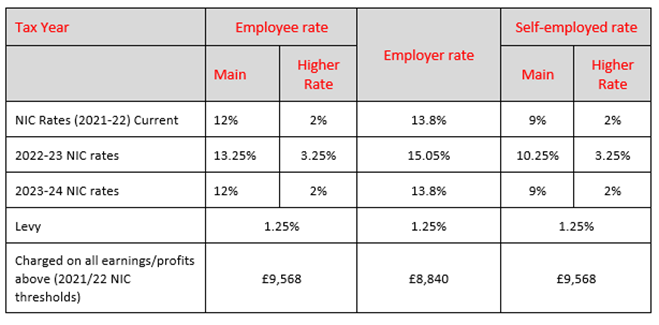

From April 2022 (2022/23 Tax Year) – There will be a temporary 1.25% increase in Class 1 (employee) and Class 4 (Self-employed) National Insurance contributions (NIC) paid by workers, as well as a 1.25% increase in Class 1 secondary NIC paid by employers (so a total increase of 2.5% in respect of employed workers split 50:50 between the employer and employee). The 1.25% increase will also apply to Class 1A and Class 1B NIC paid by employers.

The increase will apply to employed (including deemed employees) and self-employed individuals and partners earning above the Class 1 primary threshold/Class 4 lower profits limit (currently £9,568 in 2021/22). Employers will pay the additional 1.25% for employees earning above the Class 1 secondary threshold (currently £8,840 in 2021/22).

Existing reliefs and allowances from employers’ secondary Class 1 NICs will apply to the levy, including the £4,000 employment allowance, reliefs for employers of apprentices, newly employed veterans, and new employees in freeports.

Health & Social Care Levy rates : Increase to National Insurance rates from April 2022

From April 2023 (2023/24 Tax Year) – The increases will be legislated separately as a ‘health and social care levy’ and NIC rates will return to 2021/22 levels. The levy will be hypothecated in law, meaning that the revenues will be ringfenced for health and social care. From 2023 it will also apply to individuals above State Pension age who are employed or self-employed, who are currently exempt from paying NIC.

The levy, including the temporary NIC increase in 2022, is to be legislated for shortly.

The Levy will be administered by HMRC and collected by the current channels for NICs – PAYE and Income Tax Self-Assessment and apply to earnings/profits above the respective NIC thresholds in future years, as determined by the government and announced by the Chancellor in the budget each year.

Dividend tax increase

As well as the levy, to be paid by employees, the self-employed and employers, the Government has announced a 1.25% increase in dividend tax rates from April 2022, taking rates to 8.75% for basic rate taxpayers, 33.75% for higher rate taxpayers and 39.35% for additional rate taxpayers. The £2,000 dividend allowance will remain. Dividends earned within an individual Savings Account (ISA) are excluded from dividend tax.

The increase in dividend tax rates will be legislated for in the next Finance Bill.

From April 2022: Dividend tax rates in all bands will increase by 1.25%, as shown below:

Please see our Health and Social Care Levy document for clear examples of both the NI and Dividend tax increases, click here to view or download

The tax raising measures are outlined in HM Government Build Back Better – Plan for health and social care. click here

If you would like help or advice on this or any other tax issue, please do not hesitate to contact us.